With the RBI spending over $100 billion defending the rupee, oil shocks widening the import bill, and foreign capital turning cautious, India’s growing external vulnerability may now require more than public appeals — it may demand a permanent institutional external stability framework.

By Ravishankar Kalyanasundaram

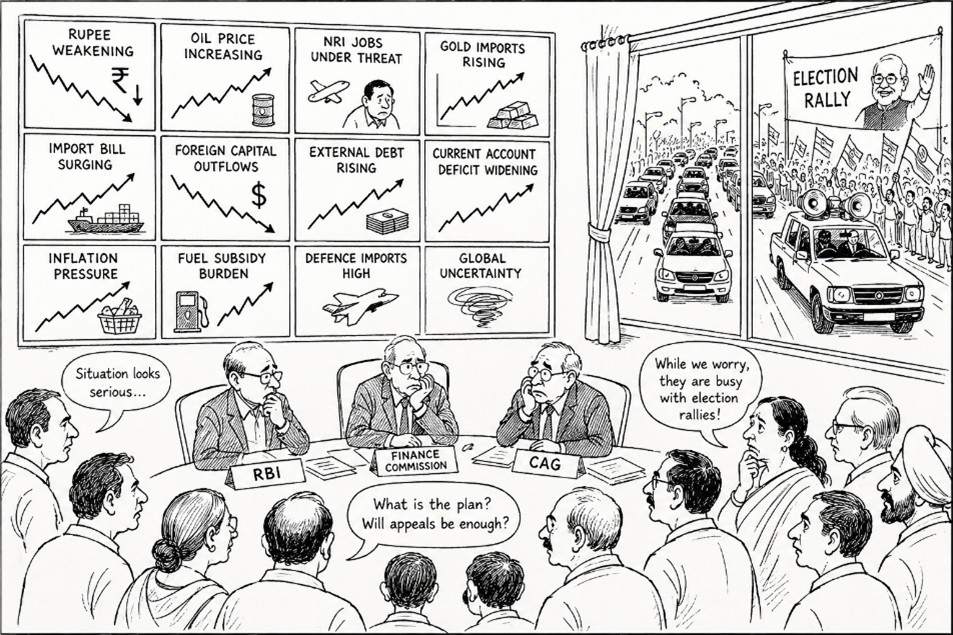

Prime Minister Narendra Modi’s public appeal asking citizens to conserve fuel, postpone unnecessary foreign travel and reconsider gold purchases should not be seen as a routine advisory. The pressure underneath is serious. And the response now required must go far beyond appeals from public platforms.

Because what India is witnessing today is not routine currency volatility.

Spending over $100 billion in barely over a year to defend the rupee is not normal currency management. The Reserve Bank of India is fighting a prolonged defensive battle in the currency markets.

How long can this continue?

The once formidable foreign exchange reserve position of nearly $728 billion is today less fortified than it appears because relentless import pressure continues to drain the system from multiple directions. Importing over 5 million barrels of crude oil every single day, India simply cannot afford to ignore global oil price movements. Every $10 increase in crude prices increases India’s annual import bill by more than $15 billion. That burden rapidly spreads into transport costs, fertiliser subsidies, electricity generation, manufacturing expenses and inflation itself.

And oil is only one part of the story.

Gold imports continue at over $50 billion annually. Electronics imports remain massive. Semiconductor-linked components, defence procurements, industrial machinery and edible oil all require dollars. Fertilisers and edible oil imports continue. Overseas tourism and foreign education continue drawing billions of dollars outward every year.

Not that India can ban any of these. That is precisely why the situation deserves far greater seriousness and institutional attention.

Because while the outflows continue relentlessly, even the inflows are beginning to show signs of vulnerability.

Remittances from Indians abroad remain critical to India’s external stability. Yet sectors employing large Indian workforces overseas are themselves facing uncertainty from slowing global growth and geopolitical instability. Foreign portfolio investments too have become increasingly volatile amid elevated US bond yields, geopolitical tensions and a strengthening dollar environment. Global investors are becoming defensive. Capital is moving toward safety and liquidity.

Every one of these developments directly pressures the rupee.

Yet India’s response still appears fragmented, reactive and unusually mild for the scale of the challenge emerging underneath.

A public appeal to conserve dollars cannot become the country’s principal response to a growing external vulnerability. India now requires a visible and permanent institutional framework continuously monitoring and communicating the country’s external position.

The situation cannot be dismissed as a temporary or passing phase. It is becoming a mirror reflecting deeper structural vulnerabilities within the Indian economy. India wants to become a manufacturing superpower, but remains deeply dependent on imported energy, imported electronics, imported components and imported capital. We celebrate rising consumption, but rarely ask whether that consumption is externally sustainable during geopolitical stress. We celebrate growing air travel and overseas tourism, but ignore the growing dollar leakage accompanying them. We encourage digital growth while importing massive volumes of electronics and semiconductor-linked components.

This is no longer merely an RBI issue.

What India perhaps requires now is a permanent high-powered External Stability Council consisting of the RBI, Finance Ministry, Finance Commission and Comptroller and Auditor General to periodically review and publicly communicate the country’s external vulnerability, reserve adequacy, state borrowings, import intensity, sovereign obligations and dollar exposure. Such an institutional mechanism should issue periodic advisories, publish structured external vulnerability assessments and initiate coordinated responses across sectors before pressures become destabilising.

India already watches every Monetary Policy Committee announcement with enormous attention. But perhaps the country now needs an equally visible institutional mechanism focused exclusively on external stability and dollar vulnerability. States, industries, financial markets and trade bodies should be periodically informed of emerging pressures instead of depending upon occasional public appeals and scattered policy signals.

Because what is unfolding is larger than monetary policy.

The rupee is slowly becoming a national economic security indicator.

And when the Prime Minister himself publicly asks citizens to conserve dollars, the Government must now move decisively beyond appeals toward a visible, coordinated and institutional national response.

Business and Economy

Business and Economy  Education

Education  Food

Food  Government

Government  Lifestyle

Lifestyle  Politics

Politics  Travel

Travel  World

World