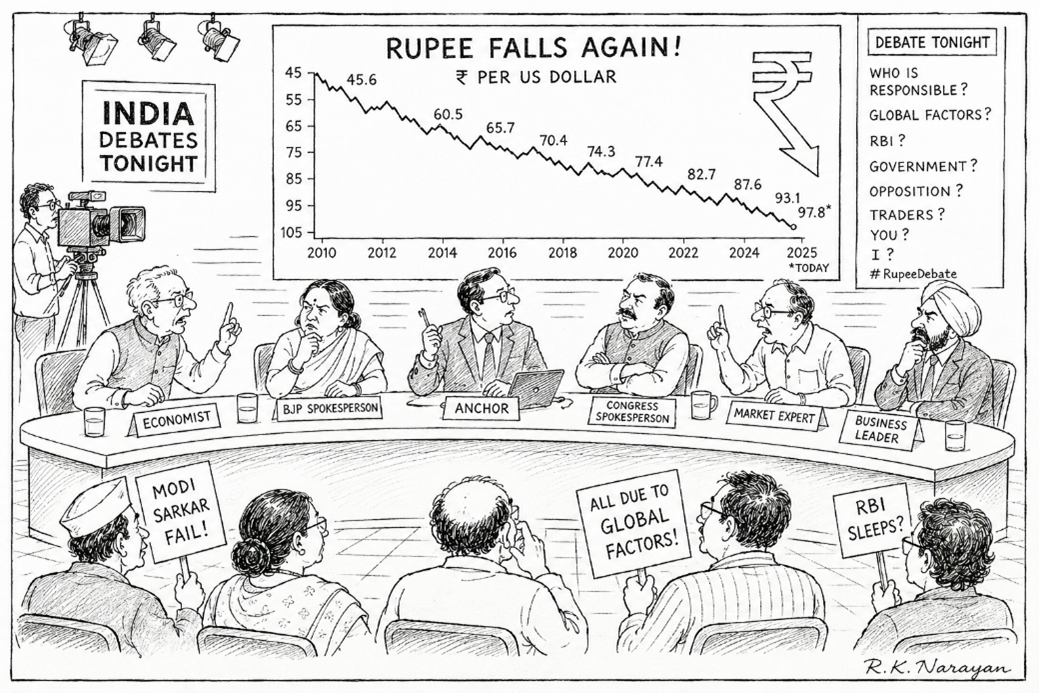

Every fall of the currency is quietly asking questions that politics often avoids.

By Ravishankar Kalyanasundaram

Over long periods of time, currencies reveal something much deeper than exchange rates or market fluctuations. They reveal the structural confidence that the world places in an economy.

And that is where India must pause and think with honesty.

For decades, India has celebrated growth with enormous pride. New highways stretching across states. Record GST collections. Rising stock markets. Digital revolutions. Startup unicorns. Metro rail networks. Mega infrastructure announcements. Airports. Expressways. Data centres. Smart cities.

All of these are important. Some are genuinely transformational. They have changed the visual landscape of India and improved the confidence of citizens.

But somewhere beneath these visible signs of progress, another quieter story has continued unfolding.

India imports nearly 85 percent of its crude oil requirement. Nearly 60 percent of its edible oil. Large volumes of electronics. Mobile phone components. Semiconductor-linked technologies. Solar equipment. AC compressors. Critical minerals. Advanced defence systems.

Every time global tensions rise, India begins worrying about the same set of issues. Oil prices. Dollar availability. Imported inflation. Foreign capital flows. Currency pressure.

And that should concern us deeply.

Because it means the economy still remains externally vulnerable in ways that are not fully visible during normal times.

The Rupee exposes this vulnerability more honestly than politics.

Politics can postpone uncomfortable conversations. Currencies cannot.

A falling currency quietly tells citizens that the country is consuming more global value than it is structurally creating.

This is not about blaming one government or another. The problem is older and deeper.

Over decades, India gradually became comfortable with an import-supported consumption economy. As incomes rose, imports rose. As aspirations rose, imports rose. As urban lifestyles expanded, imports rose.

The nation celebrated malls, smartphones, air-conditioners, edible oil abundance and cheap manufactured goods without fully asking how much of this ecosystem was actually being built inside India.

Much of our development therefore became consumption-led rather than production-deep.

The visible India became stronger. The structural India often became weaker.

We built more roads to move imported goods faster.

We expanded retail ecosystems without adequately expanding industrial ecosystems.

We celebrated demand growth while remaining dependent on foreign supply chains for many of the products driving that demand.

This imbalance remained hidden because the world remained relatively stable for long periods.

Then suddenly the world changed.

Wars broke out. Oil crossed dangerous levels. Shipping routes became vulnerable. The dollar strengthened. Supply chains fractured. Global capital became nervous.

And overnight, vulnerabilities that were hidden inside containers, ports, trade balances and corporate supply chains began appearing inside currency markets.

The Rupee then started speaking.

Not emotionally. Not politically. Mathematically.

A weak currency affects everything. Fuel becomes costlier. Transport costs rise. Food inflation spreads. Imports become expensive. Government borrowing pressures increase. Corporate balance sheets tighten. Middle-class purchasing power weakens. State finances become stressed.

And slowly, anxiety spreads through the economy even before people fully understand the source of the discomfort.

The uncomfortable truth is that India’s major economic anxieties have repeatedly carried a foreign exchange dimension beneath them. The 1991 crisis was fundamentally a dollar crisis. Oil shocks repeatedly destabilised the economy. Capital outflows repeatedly pressured the Rupee. Even today, a conflict in West Asia can influence Indian inflation faster than many domestic policy announcements.

Yet our national conversations often remain trapped in short-term politics while structural vulnerabilities continue expanding quietly underneath.

What makes this even more worrying is that India is often slow in taking difficult strategic decisions that are essential for long-term resilience.

The country pauses endlessly on issues that directly affect self-reliance.

Copper mining projects become trapped in years of protests, legal battles and political hesitation, forcing larger import dependence in a world where electrification, EVs and energy transition require massive copper availability.

Edible oil tells an even more painful story.

India once had the agricultural capability, climate advantage and rural labour strength to become a major edible oil producer. Instead, over decades, policy inconsistency, weak incentives and fragmented execution allowed imports to surge dramatically. Today the country spends enormous amounts of foreign exchange importing palm oil, soybean oil and sunflower oil while millions of acres of rural economic opportunity remain underdeveloped.

The same pattern repeats elsewhere.

India imports large volumes of electronic components while aspiring to become a digital superpower. We speak of AI leadership while depending heavily on imported semiconductor ecosystems. We discuss renewable energy transitions while relying substantially on imported solar modules and critical minerals.

None of this means India lacks capability.

The tragedy is almost the opposite.

India possesses enormous entrepreneurial talent, engineering capability, agricultural depth, demographic strength and market scale. In many sectors, the country could potentially become a major exporter over time if policy execution remained steady, coordinated and politically courageous.

But self-reliance is difficult work.

It requires patient coordination between Delhi, state governments, industry, farmers, financial institutions and citizens. It requires difficult land decisions, mining decisions, agricultural reforms, industrial incentives and long-term planning that survives political cycles.

Delhi alone cannot solve this. The RBI alone cannot solve this.

No central institution can permanently protect the Rupee if structural dependencies continue widening underneath the economy.

This requires a much deeper national mobilisation.

State governments must become active participants in reducing external vulnerabilities. Regions must identify strategic sectors where India can build manufacturing depth. Citizens must begin understanding that economic resilience matters as much as visible consumption growth.

Because the next phase of India’s development may not merely depend on how much the country consumes.

It may depend on how much the country can sustainably produce, secure and control.

The world itself is changing rapidly. Nations are increasingly moving away from blind globalisation towards strategic resilience. Countries are securing semiconductor ecosystems, critical minerals, food systems, energy chains and manufacturing capacities.

The global question is no longer merely:

“What is cheapest?”

It is increasingly becoming:

“What is too dangerous to remain dependent on others for?”

India cannot remain outside this transition.

The challenge before the country is therefore not simply economic. It is civilisational.

Can India become a genuinely resilient major power while remaining structurally dependent on imported energy, imported technology, imported electronics and imported strategic materials?

Or must the Republic now move from superficial growth towards deeper national capability?

Perhaps that is what the Rupee has been trying to tell us all along.

Quietly. Patiently. Without ideology.

Every fall in the currency is not merely a market event.

It is a warning signal from the deeper foundations of the economy.

And nations that ignore such signals for too long eventually discover that currencies are often more honest than politics.

Business and Economy

Business and Economy  Education

Education  Food

Food  Government

Government  Lifestyle

Lifestyle  Politics

Politics  Travel

Travel  World

World