How “true and fair” are the balance sheets we read today? When wars alter markets overnight, cyberattacks disrupt entire industries and artificial intelligence reshapes business models faster than assets can be depreciated, can accounting and audit frameworks designed for a more predictable age continue to provide the assurance stakeholders expect?

By Ravishankar Kalyanasundaram

How “true and fair” are the balance sheets that we read today?

The question may appear uncomfortable, even provocative. Yet it deserves serious consideration. For generations, investors, lenders, regulators and boards have relied upon audited financial statements as the most authoritative representation of an enterprise’s financial position. The concept of a “true and fair view” has been the cornerstone upon which confidence in financial reporting has been built.

But what if the world within which those concepts evolved has fundamentally changed?

Most accounting and auditing frameworks were developed during an era when economic change was relatively gradual. Risks moved slowly. Supply chains were largely predictable. Technological disruption occurred over years rather than months. Geopolitical events influenced markets, but seldom transformed entire industries overnight. Management assumptions, while imperfect, generally survived long enough for financial statements to remain relevant well beyond the date on which they were signed.

Today’s world bears little resemblance to that environment.

The COVID-19 pandemic demonstrated how quickly economic reality can shift. Businesses that appeared financially robust suddenly found revenues evaporating, customers disappearing and supply chains collapsing within weeks. Inventories that had been valued with confidence became difficult to sell. Receivables that appeared collectible became uncertain. Assets expected to generate returns for years suddenly faced questions about their commercial viability. A virus that never appeared in a chart of accounts ultimately rewrote balance sheets across the world.

The Russia-Ukraine conflict provided another lesson. What began as a geopolitical event quickly altered energy prices, commodity costs, freight rates, inflation expectations and industrial economics. Companies located thousands of miles away from the battlefield found their margins compressed, their forecasts revised and their assumptions challenged. A military conflict had travelled directly into corporate balance sheets.

Technology has introduced another dimension of uncertainty. Artificial intelligence is already reshaping industries at a pace few anticipated. A company may invest heavily in facilities, systems or business models expected to remain productive for decades. Yet a technological breakthrough elsewhere in the world can fundamentally alter demand patterns and competitive economics long before those assets reach the end of their accounting life. The asset may remain physically useful while becoming economically obsolete.

Cybersecurity has become equally significant. The cyberattack on MGM Resorts in 2023 reportedly resulted in losses exceeding US$100 million and disrupted operations across hotels, gaming facilities and customer services. What initially appeared to be a technology problem quickly became a revenue problem, a customer problem, a liquidity problem and ultimately a governance problem. A cyber incident had become a financial event.

These developments reveal an important reality. Events that appear entirely unrelated to accounting increasingly travel across balance sheets with extraordinary speed. A cyberattack can alter assessments of materiality and business continuity. A geopolitical event can transform inventory valuations. Trade sanctions can affect receivables. Technological disruption can create impairment risks. What were once viewed as isolated external events are now capable of influencing the financial position of enterprises almost immediately.

This raises a profound question for the accounting and auditing profession. If the nature of risk has changed so dramatically, can the frameworks used to assess those risks remain unchanged? More importantly, should institutions responsible for financial assurance learn from the realities of the modern world and evolve accordingly?

The issue is not whether auditors are complying with standards. Most do. Nor is the issue whether accounting principles remain important. They undoubtedly do. The challenge lies elsewhere. Stakeholders today are increasingly concerned not merely with whether numbers are accurate, but whether the assumptions beneath those numbers remain resilient.

This distinction matters enormously.

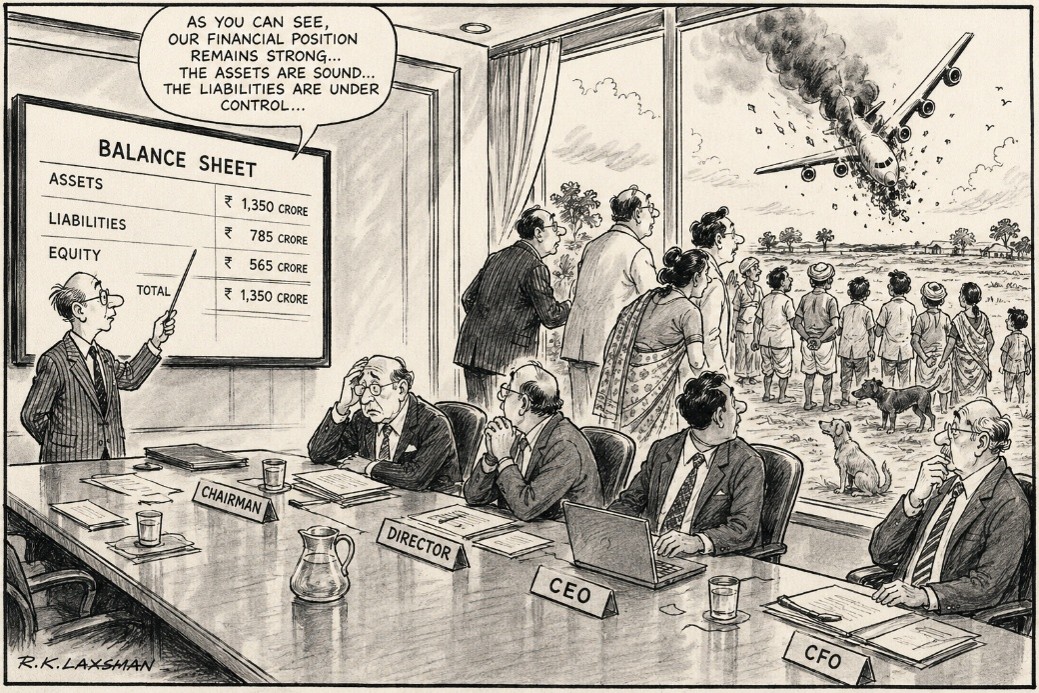

A balance sheet can comply fully with accounting standards and yet remain vulnerable to developments that were never adequately contemplated. A business may report profits while remaining exposed to a single supply chain, a single technology platform, a single geography or a single geopolitical risk. The numbers may be technically correct while the enterprise itself is becoming increasingly fragile.

This is why boards around the world are spending more time discussing resilience than they did a decade ago. Supply-chain concentration, cybersecurity, geopolitical exposure, energy security, technology disruption and scenario planning have moved from the margins of governance discussions to the centre of boardroom deliberations. Investors too are asking broader questions about sustainability, adaptability and long-term durability.

The auditing profession therefore stands at an important crossroads. Its future may depend not merely on verifying historical accuracy but on developing a deeper understanding of organisational resilience. This does not mean auditors should become strategists, economists or geopolitical analysts. It does mean, however, that the profession can no longer afford to ignore the environment within which financial statements are created.

Perhaps the most important challenge facing audit today is not compliance but relevance. Can assurance remain meaningful if it focuses primarily on historical transactions while the greatest threats to enterprise value emerge from rapidly evolving external events? Can “true and fair” continue to mean the same thing in a world where assumptions can be overtaken by events almost overnight?

These are not questions for auditors alone. They are questions for regulators, standard setters, boards, investors and business leaders. Institutions that have served markets well for decades must now ask whether they are adapting quickly enough to the realities of a world defined by uncertainty, interconnected risks and accelerating change.

The question is no longer whether disruption will occur. The question is whether our systems of financial reporting and assurance are evolving rapidly enough to recognise the disruption that is already unfolding around us.

Because in today’s world, the greatest threat to a balance sheet may not be an arithmetic error.

It may be an assumption that belonged to a world which no longer exists.

Business and Economy

Business and Economy  Education

Education  Food

Food  Government

Government  Lifestyle

Lifestyle  Politics

Politics  Travel

Travel  World

World