As the MPC signals stability, India’s real risks — capital constraints, energy shocks, employment stress and volatile global flows — demand a broader, coordinated response.

By Ravishankar Kalyanasundaram

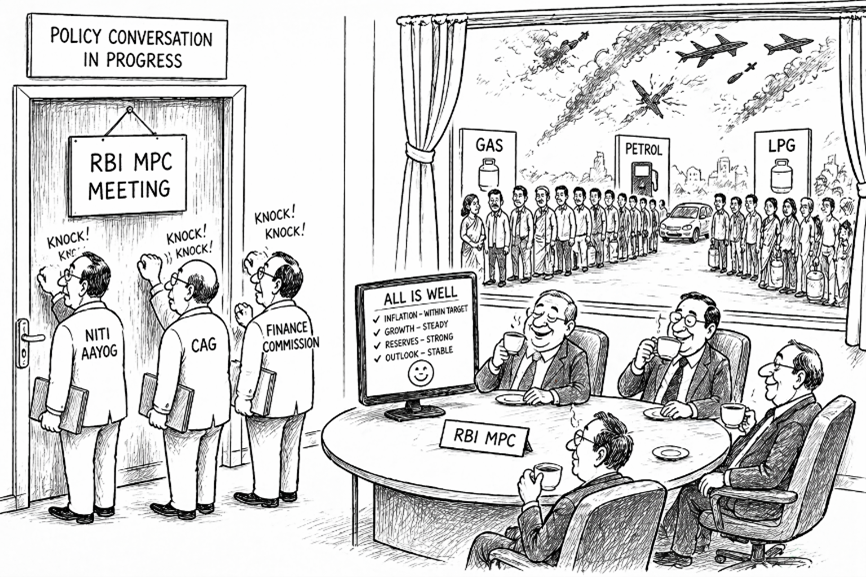

The latest meeting of the Reserve Bank of India’s Monetary Policy Committee ended as expected. Inflation within tolerance. Growth steady. Stance calibrated.

On paper, stability.

But step outside that frame, and the questions begin.

What, today, is the purpose of the MPC?

If it is to anchor inflation expectations and signal continuity, it has done so. But if the economy it serves is now more exposed, more interconnected, and more vulnerable to simultaneous shocks, is that purpose still enough?

Because the risks outside the MPC room are not waiting.

Has the MPC addressed the ₹100 lakh crore infrastructure ambition and the visible strain in long-term financing? When capital tightens and projects slow, who aligns liquidity with national priorities?

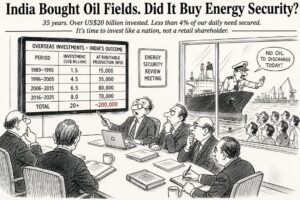

Has it addressed energy vulnerability? With nearly 85% dependence on imported crude, can inflation be viewed in isolation from geopolitical risk? If oil prices surge, if LPG costs strain households and small enterprises, who is anticipating that transmission?

Has it addressed the fragility of external flows? Over $100 billion in remittances underpin consumption. FDI is moderating. Global capital is selective. If these flows weaken, who connects the dots to demand, investment, and currency stability?

Has it addressed exports in a world of shifting supply chains and uncertain demand? If India risks marginal positioning in new trade corridors, where is the coordinated response?

Has it addressed employment — not as an outcome of growth, but as a central concern? When millions enter the workforce each year and jobs remain uneven, where does this reality sit in policy?

Because the deeper discomfort is now visible.

The comfort indicators and the risk indicators are moving in different directions.

Inflation is contained — but energy risks are rising.

Growth is steady — but employment remains uncertain.

Reserves are comfortable — but capital flows are volatile.

Ambitions are expanding — but financing is uneven.

Each thread pulls at the others.

If infrastructure financing falters, growth slows, employment weakens, and banking stress rises.

If energy prices surge, inflation accelerates, fiscal deficits widen, and consumption contracts.

If external flows tighten, currency stability is tested, capital costs rise, and investment decisions are deferred.

These risks are not sequential.

They are simultaneous.

And yet, policy remains compartmentalised.

The NITI Aayog speaks of strategy. The Finance Commission of India shapes fiscal architecture. The Comptroller and Auditor General of India ensures accountability. The RBI manages monetary stability.

Each performs its role with discipline.

But who is responsible for convergence?

Who is asking the integrated question — not just what is happening to inflation, but what is happening to the economy as a whole?

And if the MPC is not designed to address these broader trends, then what is?

Should the MPC evolve — not by diluting its mandate, but by broadening its field of vision?

Should it become a forum where inflation is read alongside energy risk, where growth is tested against employment, where liquidity is aligned with infrastructure financing?

Should it engage structurally with NITI Aayog, the Finance Commission, and the CAG — not occasionally, but as part of its design?

Or do we need something more — an institutional mechanism that sits above these silos and forces convergence?

Because the cost of inaction is not abstract.

It shows up in delayed projects, rising input costs, hesitant investment, uncertain jobs, and a gradual erosion of economic confidence.

There is a quiet urgency beneath this surface of stability.

An economy where signals are diverging. Where comfort in one indicator masks stress in another. Where policy risks becoming precise, but incomplete.

The MPC has delivered what it was meant to deliver.

The question is whether that is still enough.

If not the MPC, then who?

And if not now, when?

Business and Economy

Business and Economy  Education

Education  Food

Food  Government

Government  Lifestyle

Lifestyle  Politics

Politics  Travel

Travel  World

World