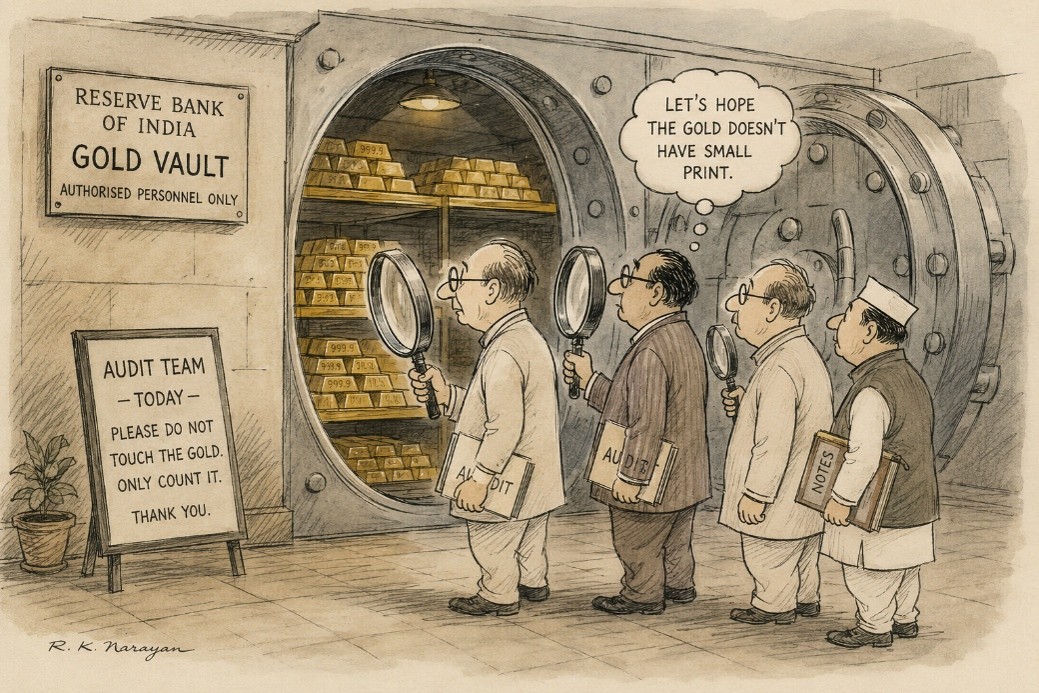

India’s Gold Reserves Are Safe, Says the RBI. But Who Counts the Bars?

By Ravishankar Kalyanasundaram

The Reserve Bank of India recently dismissed rumours that it had sold part of India’s gold reserves. The clarification was swift and reassuring. India’s official gold holdings, now exceeding 880 tonnes, remain intact.

Yet the episode leaves behind a more interesting question.

If gold is one of the most important assets on the nation’s balance sheet, where exactly is it stored? Who verifies that it exists? How often is it physically checked? And how much confidence should citizens place in the number that appears each year in the RBI’s accounts?

Most people assume India’s gold sits entirely inside a heavily guarded vault somewhere in Mumbai. In reality, the story is more complicated. Around three-quarters of India’s gold is now held domestically in RBI vaults, while the balance remains with overseas custodians, principally the Bank of England and the Bank for International Settlements. Over the past few years, India has quietly brought back substantial quantities of gold from overseas locations, reflecting a broader trend among central banks to keep strategic assets closer to home.

The shift is not difficult to understand. The freezing of Russian reserves following the Ukraine conflict reminded governments that assets held abroad may legally belong to them, but access to those assets can become entangled in geopolitics.

This naturally raises the question of verification.

The RBI’s gold holdings form part of its audited balance sheet and are subject to internal controls, reconciliation procedures and audit processes. Gold held overseas is supported by confirmations from custodial institutions. Yet neither the RBI Annual Report nor public audit disclosures provide detailed information regarding the dates of physical verification, the quantities inspected or the methodology adopted.

From an accounting perspective, this is not unusual. Most central banks operate in a similar manner. Yet from a citizen’s perspective, curiosity remains. If auditors physically verify inventories in factories, warehouses and ports, it is reasonable to ask how often the nation’s gold receives the same attention.

India is hardly alone in confronting such questions.

The United States officially holds more than 8,100 tonnes of gold, much of it associated with the legendary Fort Knox vault. Yet for decades politicians, economists and journalists have periodically demanded fresh inspections and greater transparency. The issue is not that anyone seriously believes the gold has disappeared. Rather, gold occupies a unique place in the public imagination. Unlike bonds or foreign currency reserves, it can be touched, weighed and counted.

Italy recently experienced a different kind of controversy. Home to the world’s third-largest gold reserves, Italy became embroiled in a political debate over who actually owns the gold. Some lawmakers argued that the reserves belonged directly to the Italian people rather than the central bank. The gold itself was never in doubt. The argument was over sovereignty, control and accountability. Even in advanced economies, gold has a habit of moving from the vault into the political arena.

India understands the symbolism of gold perhaps better than most nations. In 1991, when the country faced a severe balance-of-payments crisis, 67 tonnes of gold had to be pledged abroad to secure emergency funding. The episode became a powerful symbol of economic vulnerability. Today’s reserve position tells a very different story. India now ranks among the world’s major gold holders and continues to strengthen its reserve buffers.

Yet the larger question remains relevant.

Gold is unique because it combines finance, politics and psychology. A government bond is trusted because a government stands behind it. Gold is trusted because it simply exists. That is why central banks continue to accumulate it despite the rise of digital currencies, artificial intelligence and sophisticated financial instruments.

The RBI’s assurance that India’s gold remains intact should reassure markets. But the discussion serves a useful purpose. It reminds us that trust in public institutions ultimately rests not only on ownership of assets but also on transparency regarding their custody and verification.

After all, gold may be stored in vaults, recorded in balance sheets and protected by security systems. But confidence in those numbers is stored somewhere else entirely.

It resides in the credibility of the institutions that guard them.

Business and Economy

Business and Economy  Education

Education  Food

Food  Government

Government  Lifestyle

Lifestyle  Politics

Politics  Travel

Travel  World

World