For three decades India pursued oil fields from Russia to Venezuela, spending billions in search of energy security. The results reveal important successes, costly lessons and a pressing need to rethink how a nation secures its future energy supplies.

By Ravishankar Kalyanasundaram

A recent meal with a good friend from the oil and gas industry left me reflecting on a question that India can no longer afford to ignore.

Having spent decades in the sector, he has witnessed India’s overseas energy investments evolve from their earliest days. As we discussed oil markets, geopolitics and India’s growing dependence on imported energy, he made an observation that struck me immediately.

“We measure overseas investments by dollars spent and reserves acquired,” he said. “But a nation should measure them by barrels secured.”

He then posed a question that remained with me long after lunch had ended.

“After spending more than US$20 billion over three decades, how many barrels of energy security has India actually bought?”

The answer tells an important story about both the successes and shortcomings of India’s energy strategy.

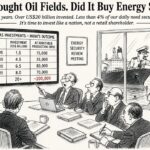

India’s overseas energy journey began in earnest after the establishment of ONGC Videsh in 1989. Over the next thirty-five years, Indian public sector energy companies invested across Russia, Venezuela, Sudan, South Sudan, Vietnam, Azerbaijan, Mozambique and the Middle East. The rationale was compelling. India’s economy was expanding rapidly, domestic production was proving inadequate and dependence on imported crude was steadily increasing. If India could not discover sufficient reserves at home, it would acquire them abroad.

The logic remains sound even today.

What deserves examination is not the intent but the outcome.

India currently consumes approximately 5.8 million barrels of oil every day. Domestic production contributes only about 700,000 barrels per day. Nearly five million barrels therefore have to be imported every single day to keep the economy functioning. Against this requirement, the entire overseas production attributable to Indian investments is estimated at roughly 200,000 barrels per day.

That single number should command attention.

After investing more than US$20 billion over three and a half decades, India’s overseas oil portfolio secures less than four percent of the country’s daily requirement.

This is not a story of failure. Many investments were made under circumstances that justified the decisions at the time. Several have generated production, profits and strategic value. Yet it is difficult to argue that a portfolio covering less than four percent of national demand represents the level of energy security a country of India’s scale requires.

The strongest investments have undoubtedly been in Russia. Sakhalin-1 contributes an estimated 35,000 to 40,000 barrels per day attributable to India, while the Vankor and Taas-Yuryakh assets contribute another 60,000 to 70,000 barrels per day. These investments have generated meaningful production and remain among the most successful overseas acquisitions undertaken by Indian energy companies.

Yet even these successes reveal the scale of India’s challenge. The combined contribution from some of India’s best-performing overseas assets covers only a few hours of national oil consumption. The issue is therefore not whether the investments worked. The issue is whether they worked at a scale sufficient to alter India’s vulnerability.

The Venezuelan experience illustrates the point even more sharply. India invested close to US$1 billion in projects that were expected to provide long-term access to one of the world’s richest hydrocarbon provinces. Today India’s attributable share of production from those investments is estimated at roughly 4,000 to 5,000 barrels per day. In practical terms, nearly two decades of investment provide enough oil to satisfy less than thirty minutes of India’s daily consumption. The reserves exist. The energy security does not.

Mozambique tells a different but equally important story. Indian companies invested heavily in what remains one of the world’s most promising LNG developments. The resource base is substantial and the long-term potential remains attractive. Yet security concerns and insurgency have delayed development for years. Billions have been committed, but the strategic benefits have yet to materialise.

As my friend observed during our discussion, the problem was rarely geology. The oil was often there. The gas was often there. The challenge was that India frequently acquired financial interests rather than strategic control.

This distinction is crucial.

A retail investor buys shares seeking returns. A nation acquires overseas energy assets seeking resilience. The purpose is not merely to earn dividends. The purpose is to ensure that when wars erupt, sanctions are imposed, shipping lanes are disrupted or geopolitical tensions escalate, energy continues to reach domestic consumers.

Measured against this objective, India made several mistakes.

The first was focusing on reserves acquired rather than barrels secured. Annual reports celebrated acreage, reserves and investments. The more important question often remained unanswered. How much oil can India actually count on during a crisis?

The second was acquiring minority stakes without sufficient operational influence. In many cases India became a financial participant rather than a strategic owner. The reserves partially belonged to India, but critical decisions frequently remained under the control of others.

The third was viewing upstream investments in isolation. Energy security does not begin and end at the oil field. It extends through shipping, storage, refining, trading and strategic reserves. India acquired assets, but often failed to build the integrated systems required to transform those assets into reliable security.

The fourth was a lack of scale. India diversified across multiple geographies, which reduced concentration risk, but the resulting portfolio remained too small relative to the country’s enormous requirements.

This is where the comparison with China becomes instructive.

Chinese state-owned energy companies pursued overseas investments as part of a broader national strategy. Investments in Russia, Kazakhstan, Iraq, Angola, Brazil and the Middle East were integrated with pipelines, shipping fleets, strategic petroleum reserves, refining assets and long-term supply agreements. China’s overseas equity oil production today exceeds two million barrels per day, roughly ten times India’s overseas entitlement.

The difference is not merely financial.

The difference is strategic.

China invested as a nation building an energy security architecture. India often invested as an owner of assets.

Fortunately, there are signs that India may already be moving in a more strategic direction.

The evolving partnership with the UAE is particularly encouraging. Indian companies have acquired stakes in producing and exploration assets in Abu Dhabi. More importantly, cooperation now extends to strategic petroleum reserves, storage facilities, LNG infrastructure and long-term supply arrangements. This is significant because it focuses not merely on ownership of reserves but on ownership of outcomes.

The UAE model deserves careful study because it addresses many of the shortcomings of the past. It combines production, logistics, storage and long-term supply relationships within a stable geopolitical framework. This is far closer to what a modern energy security strategy should look like.

The next phase of India’s overseas energy investments should therefore be guided by a different philosophy.

Every project should be evaluated by a simple metric: how many barrels per day are secured for India?

Future investments in Guyana, Brazil, the UAE, Saudi Arabia, Oman and emerging producers such as Namibia should be linked to guaranteed offtake rights, shipping arrangements and strategic storage. The objective should not merely be ownership of reserves beneath foreign soil. The objective should be assured access to energy during periods of disruption.

India should also establish a clear national target. Rather than measuring success in terms of reserves acquired or dollars invested, policymakers should focus on securing at least one million barrels per day of overseas entitlement and long-term supply arrangements over the next fifteen years. Such a portfolio would cover nearly one-fifth of current imports and provide meaningful protection against future shocks.

The world is entering an era of increasing geopolitical uncertainty. Supply chains are becoming more fragile. Energy markets are becoming more politicised. Strategic competition among major powers is intensifying. In such a world, energy security cannot be left entirely to market forces.

It must be built deliberately.

India’s overseas investments over the past thirty-five years were not mistakes. They were the first chapter of a much larger story. The next chapter, however, must be written differently.

As my friend remarked while we finished lunch, “The objective was never to own a piece of an oil field somewhere in the world. The objective was to ensure that when India needs oil, the oil arrives.”

That may be the most important lesson from thirty-five years of overseas energy investments.

India bought oil fields.

What it must now buy is energy security.

Business and Economy

Business and Economy  Education

Education  Food

Food  Government

Government  Lifestyle

Lifestyle  Politics

Politics  Travel

Travel  World

World