As oil prices rise, exports slow, remittance flows face uncertainty and the rupee weakens, the RBI confronts a larger challenge than inflation — safeguarding India’s external economic resilience in an increasingly fragile world.

By Ravishankar Kalyanasundaram

As the Monetary Policy Committee meets today, much of the public discussion has narrowed itself to a familiar debate. Economists, market participants and television studios are focused on whether the Reserve Bank of India will raise interest rates, hold them steady or signal a different policy path in the months ahead. It is an important discussion, but perhaps not the one India should be having at this moment.

The larger question before the RBI is whether India can continue to generate, attract and retain the foreign exchange required to sustain its ambitions over the next two decades. This may appear unusual in the context of a monetary policy meeting, yet it lies at the heart of India’s development story. Inflation remains important. Interest rates matter. But neither can be viewed in isolation from the larger challenge of financing India’s rise in an increasingly uncertain world.

Across the country, evidence of India’s aspirations is visible everywhere. New highways stretch across states. Freight corridors are taking shape. Ports and airports are expanding. Data centres are rising on the outskirts of major cities. Renewable energy parks, semiconductor projects, logistics hubs and industrial corridors are being announced with increasing frequency. India is not merely seeking growth. It is attempting one of the most ambitious economic transformations undertaken by any nation in recent history.

Such a transformation requires enormous amounts of capital. More importantly, it requires enormous amounts of foreign exchange. Machines must be imported. Technology must be acquired. Energy must be purchased. Critical minerals, electronics, semiconductor equipment and specialised industrial inputs often have to be sourced from overseas markets. The dream may be domestic, but many of the resources required to achieve it continue to be priced in dollars.

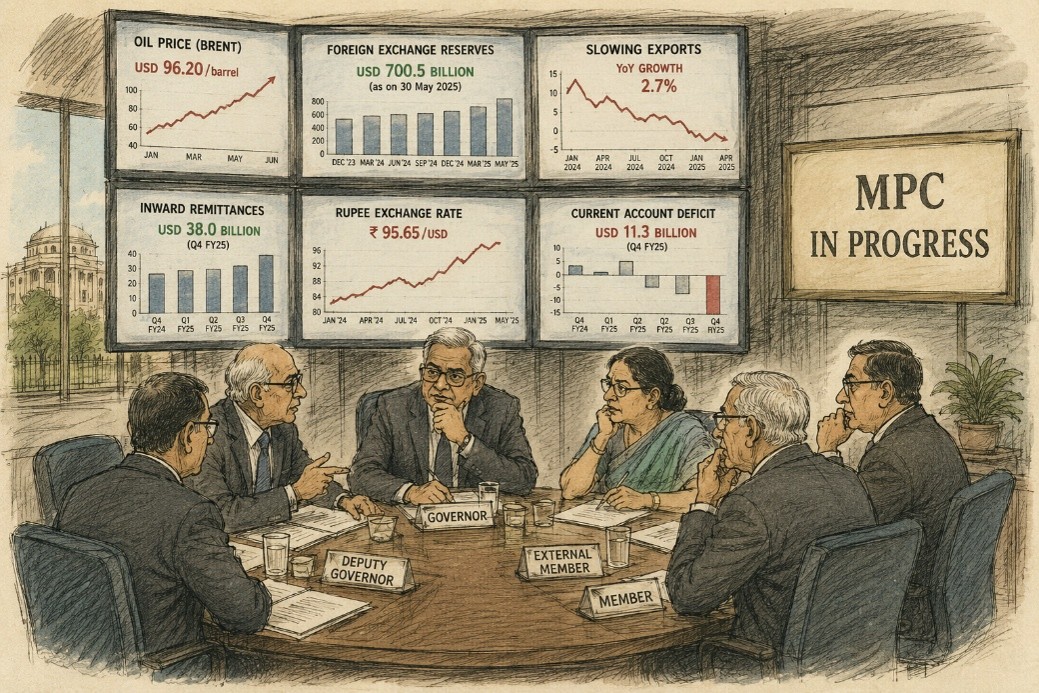

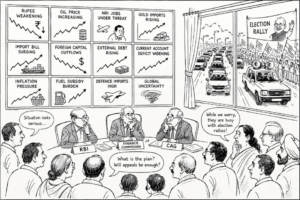

This is where the numbers begin to tell an important story. India’s merchandise exports in the last financial year were approximately $442 billion, while merchandise imports approached $775 billion, resulting in a merchandise trade deficit of more than $333 billion. Services exports continue to provide a valuable cushion and have become one of India’s greatest strengths, helping total exports reach around $860 billion. Yet total imports still exceeded $979 billion, leaving a substantial gap that must be financed through remittances, capital inflows and foreign investment.

For many years, India benefited from three dependable sources of dollars. The first was a steadily growing export sector. The second was the extraordinary contribution of millions of Indians working abroad who sent money home every month. The third was the willingness of global investors to commit capital to India’s growth story.

Today, each of these sources faces new uncertainties. Global growth is slowing. Protectionist policies are returning across many economies. Supply chains are being reshaped by geopolitical tensions. The Middle East, which remains central both to India’s energy security and remittance flows, faces recurring instability. Europe continues to struggle with weak economic growth, while the United States is increasingly focused on strengthening domestic manufacturing and strategic industries.

Even remittances, one of India’s most reliable sources of foreign exchange, cannot be viewed as permanently immune from global developments. The prosperity of Indian workers in the Gulf, North America and Europe remains linked to economic conditions in those regions. Any sustained slowdown abroad eventually finds its way into India’s external accounts.

At the same time, the nature of global capital itself is changing. The era of easy money that characterised much of the previous decade has come to an end. Investors have become more selective, more demanding and more sensitive to risk. Capital today moves across borders with remarkable speed, comparing opportunities not merely within Asia but across the entire world. Countries compete not only for investment but also for confidence.

This distinction is important because India requires a particular kind of capital. It does not merely need speculative flows that enter and exit financial markets in response to short-term opportunities. It needs patient capital capable of financing infrastructure projects whose returns may take years or even decades to materialise. The highways, ports, airports, logistics parks, renewable energy projects and digital infrastructure that India is building today require investors willing to think beyond quarterly returns and electoral cycles.

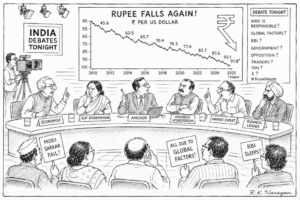

This is why the rupee matters far more than many assume. A currency is not simply a medium of exchange. It is a reflection of confidence. It captures how global investors, businesses and markets view a country’s future prospects. Every significant decline in the rupee increases the cost of imports, raises uncertainty for investors and places additional pressure on the economy’s external balances. The movement of the rupee from around ₹83 to the dollar less than two years ago to around ₹95-96 today is not merely a statistical change. It is a reminder that economic fundamentals, external vulnerabilities and investor perceptions are deeply interconnected.

India’s foreign exchange reserves, now exceeding $700 billion, undoubtedly provide comfort. They represent one of the country’s great economic achievements and offer an important buffer against external shocks. Yet reserves by themselves are not a strategy. They are a line of defence. A nation cannot indefinitely rely on its reserves without continuously replenishing them through exports, investment, innovation and competitiveness.

The question before the RBI today therefore extends well beyond inflation management. Inflation targeting has served India well and should remain an important pillar of monetary policy. However, the world that produced inflation-targeting frameworks has changed dramatically. Inflation today is increasingly shaped by forces that originate far beyond domestic demand conditions. Oil prices, geopolitical conflicts, shipping disruptions, sanctions, capital flows and exchange rate movements now influence inflation as much as interest rates do.

Few institutions are better placed than the RBI to understand these interconnected risks. The central bank sees the movement of capital, the behaviour of currency markets, the health of foreign exchange reserves, the liquidity position of the banking system and the emerging vulnerabilities in the economy’s external sector. It possesses a vantage point that no other institution enjoys.

This is why the time may have come to broaden the conversation about the RBI’s role. The country does not need the RBI to abandon inflation targeting. It needs the institution to evolve into something larger — the principal guardian of India’s external economic resilience. In a world characterised by geopolitical uncertainty, energy insecurity and increasingly competitive capital markets, the ability to anticipate vulnerabilities may prove just as important as the ability to control inflation.

The real challenge before the Monetary Policy Committee today is therefore not whether inflation will be 4 per cent or 4.5 per cent six months from now. The real challenge is whether India can build an economic framework capable of generating the dollars required to finance its aspirations over the next twenty years. That objective demands stronger exports, deeper debt markets, greater competitiveness, higher productivity and the ability to attract long-term patient capital from around the world.

India’s development journey has reached a stage where monetary policy, trade policy, industrial policy, energy security and capital flows can no longer be viewed in isolation. They are different chapters of the same story. The RBI sits at the centre of that story.

As the MPC meets today, the nation should certainly listen for signals on interest rates. But it should listen even more carefully for something larger: a recognition that India’s future prosperity depends not merely on managing inflation, but on strengthening the country’s balance sheet with the world.

For ultimately, India does not merely need lower inflation.

It needs more dollars, stronger confidence and institutions capable of safeguarding both.

Business and Economy

Business and Economy  Education

Education  Food

Food  Government

Government  Lifestyle

Lifestyle  Politics

Politics  Travel

Travel  World

World