India’s $600-billion cushion looks formidable, but the true strength lies not in the RBI’s ledger, but in what we produce, export, and save at home.

By Ravishankar Kalyanasundaram

The Sudden Jolt

Earlier this month, India’s foreign exchange reserves slipped by more than $9 billion in just a week as the Reserve Bank of India stepped in to defend the rupee against the latest volley of U.S. tariffs. A week later, the reserves clawed back $4.7 billion—not because exports surged or capital inflows returned, but simply through revaluation gains from firmer gold prices and a softer dollar.

It was a reminder that our reserves, while formidable on paper, remain vulnerable to forces beyond our control. Interventions can calm the waters for a few days, but they do not provide certainty for the long voyage. Which begs the question—quietly, without presumption—whether the legacy approach to reserves, built on stockpiling dollars and waiting for trouble, is still adequate in today’s turbulent world.

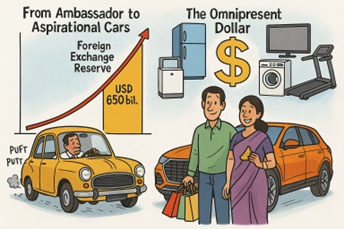

From Ambassador to Aspirational Cars

Back in the Ambassador era, India’s reserves hovered at $5–6 billion in the late 1980s—barely enough to keep petrol pumps supplied and traffic lights blinking. It matched the needs of a tightly controlled economy: restricted imports, modest aspirations, and shopping lists that rarely stretched beyond scooters, transistor radios, or the odd refrigerator.

Fast forward to today. Our roads hum with SUVs and sedans, homes are filled with imported white goods, and e-commerce delivers global brands at the click of a button. But while our shopping list is aspiring, our reserves still wheeze like that old diesel engine. With an economy deeply intertwined with the dollar, India effectively needs a far bigger limit on its national credit card—the foreign exchange reserve.

The Omnipresent Dollar

In Indian culture, God is omnipresent. Somewhere along the way, we made the dollar omnipresent too. It sits quietly in our cars, ACs, fridges, televisions, washing machines, even treadmills. Our favourite samosas, vadas, and gulab jamuns are dripping in imported edible oil—a silent but voracious dollar guzzler.

And in an era of tariff wars, supply shocks, and sanctions, the need is clear: India must earn enough dollars even as it spends them with discipline.

The Four Pillars—and Their Stress Points

India’s reserves rest on four familiar pillars.

None of these streams are collapsing, but each carries risk. Prudence demands “insurance plans” that keep flows steady no matter which pillar shakes. And as we are witnessing in the US and Europe, governments in power are increasingly driven by populist measures—many of them aimed at curbing immigration. In the Gulf too, geopolitical tensions constantly shadow the flow of people and remittances. These are ground realities, and they are beyond our control. Which is why the focus must shift to what we can control: strengthening exports, diversifying markets, and ensuring that the foundations of our reserves are rooted firmly at home.

Broadening and Deepening Our Export Base

If reserves are to be durable, the base of exporters must widen. Many of our commodity boards and export promotion councils are relics of another era; they need to be repurposed into nimble bodies attuned to today’s market.

India remains a production giant but still an export dwarf in value terms. Low-margin products like rice and buffalo meat dominate, while high-value areas are under-tapped. Agriculture, horticulture, and floriculture could scale with stronger branding, better cold chains, and predictable policy. But the story goes far beyond farms.

Recent weeks have shown the way—Japanese industries are back on Indian campuses, recruiting engineers and managers to fill their shrinking workforce. Almost every advanced economy today is short on working population, and India’s edge will come from skilling and reskilling people who can move seamlessly across borders. But the real prize is bigger: FTAs must deliver not just market access but manufacturing in India for those countries. With timely technology upgrades, world-class logistic parks, and by repurposing our SEZs and FTWZs, we can turn these opportunities into a new gold mine—feeding our foreign exchange chest with steady, sustainable dollars.

A Case in Point: Mobiles

Nowhere is this clearer than in mobiles. India did a fantastic job of attracting global manufacturers. Lakhs of jobs were created, reskilling took off, and India emerged on the global mobile map. Yet when you look under the hood, the real Indian content is modest. On $15.6 billion of phone exports last year, our net foreign exchange earning was just $3.6 billion.

A small sum, yes—but also a giant leap for a sector we barely had a decade ago. The agenda from here must be sharper: localise displays, camera modules, and battery cells; fix tariff inversion; build ATMP/OSAT facilities for chips; deepen PCB inputs; and create vendor parks with guaranteed offtake.

Beyond Phones: Engineering Exports

The same urgency must extend to engineering goods. India’s potential is vast, but much of our manufacturing is still legacy-driven. The world is racing ahead with AI, robotics, and 3D printing, while we remain at the starting blocks. We cannot afford to lose this market as we lost garments to Bangladesh and Vietnam.

A war-like plan is needed—upgrade, upskill, modernise—so that Indian engineering exports compete head-on with the best. That means money on the table: tax breaks, investment allowances, even direct grants to speed up technology adoption.

Plugging the Dollar Leaks

At the same time, we must fix obvious leaks. Why should ACs, fridges, and washing machines still rely on imported cores? Why should edible oil, once an abundant domestic product, still drain billions in forex? The policy signal must be unambiguous: within a set timeframe, these must be indigenised.

Companies that prospered from decades of easy imports must now reinvest in sesame, groundnut, sunflower, and mustard to bring smiles back to Indian farmers. And policy can go deeper still:

Every dollar saved is indeed a dollar earned.

Beyond the RBI Accountant

Foreign exchange reserves are more than a line on the RBI’s balance sheet. They mirror our industrial depth, export aggression, and policy clarity. The central banker can smooth peaks and troughs, but certainty comes from what we produce, how we export, and how we plug leaks.

Yes, the RBI is the family doctor of our reserves. But reserves are our national health card. And like any health card, it cannot improve with doctor visits alone. It reflects whether we exercise, eat right, and take care of ourselves—in economic terms: whether we export with confidence, reduce hidden imports, and localise essentials.

Towards a Broader Reserve Strategy

Today, reserve reviews are largely confined to the RBI—internal meetings, circulars, and interventions. That may have sufficed in calmer decades. But in an era of tariff turbulence, capital flight, and geopolitical shocks, a wider lens is essential.

India could benefit from a Reserve Strategy Council, bringing together NITI Aayog, the Finance and Commerce Ministries, and leading trade bodies to review the position periodically. Not to dilute the RBI’s role, but to enrich it with market intelligence, fiscal foresight, and strategic vision.

Such a mechanism would ensure course corrections are timely and collective, not just technocratic. Singapore integrates trade policy with reserve deployment; Norway invests its oil surpluses globally. India too must keep its sails trimmed to shifting winds.

A Reflective Close

India has the scale, the skills, and the ambition. The real question is whether we treat reserve management as a clerical act of stockpiling or as a national strategy of continuity. Handled wisely, reserves are not just cushions against storms; they are sails that help us catch the wind.

The RBI is the custodian of our reserves, but the content is created far beyond the Bank’s corridors. Government and industry must run the race. And to cross the line, we need not just the ledger—but hard work on the right turf.

Business and Economy

Business and Economy  Education

Education  Food

Food  Government

Government  Lifestyle

Lifestyle  Politics

Politics  Travel

Travel  World

World