When the late Lee Kuan Yew was asked by a former Maharashtra Chief Minister how Mumbai could become like Singapore, he smiled and said, “With the kind of money Mumbai sends to Delhi in taxes, you could build ten Singapores—or at least fix Mumbai.” The CM replied, “But my votes come from elsewhere. Doing that would cost me the election.” Lee later recalled it with a sigh—India’s economic decisions, he said, are hostage to re-election fears.

That observation still holds. Our fiscal devolution formula, driven by political calculus rather than economic logic, is a perfect case in point.

Yes, we know the inequity. Yes, we grumble. But this time, we urge. We want to move the needle: from discontent to diagnosis, from diagnosis to design. What we need is not quiet resignation but an alert and thinking citizenry. Not sheep to slaughter, but minds in motion. That’s what this article is for.

Let’s start with a truth: about 60% of India’s revenue comes from just a few states—Maharashtra, Gujarat, Tamil Nadu, Karnataka, and Delhi. Yet the largest shares of devolved funds go to states like Bihar, Uttar Pradesh, and Madhya Pradesh. Bihar, notably, now ranks 10th in investor base, with an emerging “equity cult,” as per a recent Business Standard report.

So why are such states still treated as chronic dependents? The current formula feels less like federalism and more like a permanent aid program—one that’s failing. Despite decades of preferential transfers, little has changed. We’ve seen populism, scandals, even state-sponsored handouts—but no deep reform.

You can blame bad governance. You can cite corruption. But here’s the rub: the formula doesn’t correct any of it—it rewards it. States that underperform continue to get more, and those that reform get less. It’s a race to the bottom, funded by the top.

The risk isn’t just fiscal imbalance. It’s broken trust in the federal architecture. If states begin deferring capital investments due to fears of inadequate returns or delay development agendas in pursuit of more favourable weights, India risks fragmenting its long-touted “one market, one tax” promise.

This is the inflection point. What India needs now is an honest examination of whether its fiscal devolution formula still serves the dynamic challenges of its states.

The Finance Commission formula—crafted to balance equity and efficiency—has remained frozen for over a decade. But India has not. Digital governance, climate volatility, technology disruptions, and geopolitical tensions have shifted the terrain.

Across the world, formulas evolve:

Formulas aren’t sacred texts; they must reflect a changing world. India’s devolution formula doesn’t. It fails to meet today’s priorities:

If we don’t adapt the fiscal framework, we invite inertia—and irrelevance.

India once needed to close a poverty gap. Today, it must close a resilience gap. Every state must ride the waves of tech churn, climate shocks, and tighter global liquidity. A Finance Commission stuck in the past can’t weather future storms.

We need a Resilience-Ready system—flexible, transparent, and reward-driven, but rooted in the spirit of federal solidarity.

Why Horizontal Distribution Still Matters—But Must Evolve Horizontal sharing is the glue of Indian federalism: without it, poorer states could never meet basic norms of schooling, roads or health. Yet today’s single-snapshot formula cannot track the moving targets of risk:

A resilience-ready system keeps solidarity but injects feedback loops: states see a clear fiscal upside in staying competitive, green and well-governed—and a downside if they drift.

After all, federal finance shouldn’t just move money around. It should move states forward.

We have come a long way from the ration-book decades—of power cuts, Lambretta lotteries, and the ‘take-it-or-leave-it’ Ambassador. Today’s India is unrecognizable in its aspirations, technology, and entrepreneurial energy.

But pause for a moment and look at the numbers. India’s combined central and state budgets today amount to nearly ₹80 lakh crore—or close to a trillion dollars. That’s larger than the total budgets of several European countries put together: Austria, Sweden, Portugal, Belgium, and Greece. Yet, do we have their infrastructure? Their public transport? Their clean cities or efficient utilities?

Why this mismatch? Consider the prices we now pay. Hotel rooms in major Indian cities rival those in Barcelona or Prague. So do branded clothes and school or college fees. Our economy is global in cost—but not always in quality.

The real problem? Indifference. Not just from the government—but from us. Policies shape our future, yet we treat them like passing trains—watched, not questioned, never boarded.

That must change. We need to speak up—through columns, forums, petitions, alumni circles. Not just post, but push. Influence must outgrow outrage. If we don’t, we risk becoming a generation that walked silently into economic decisions it never approved of.

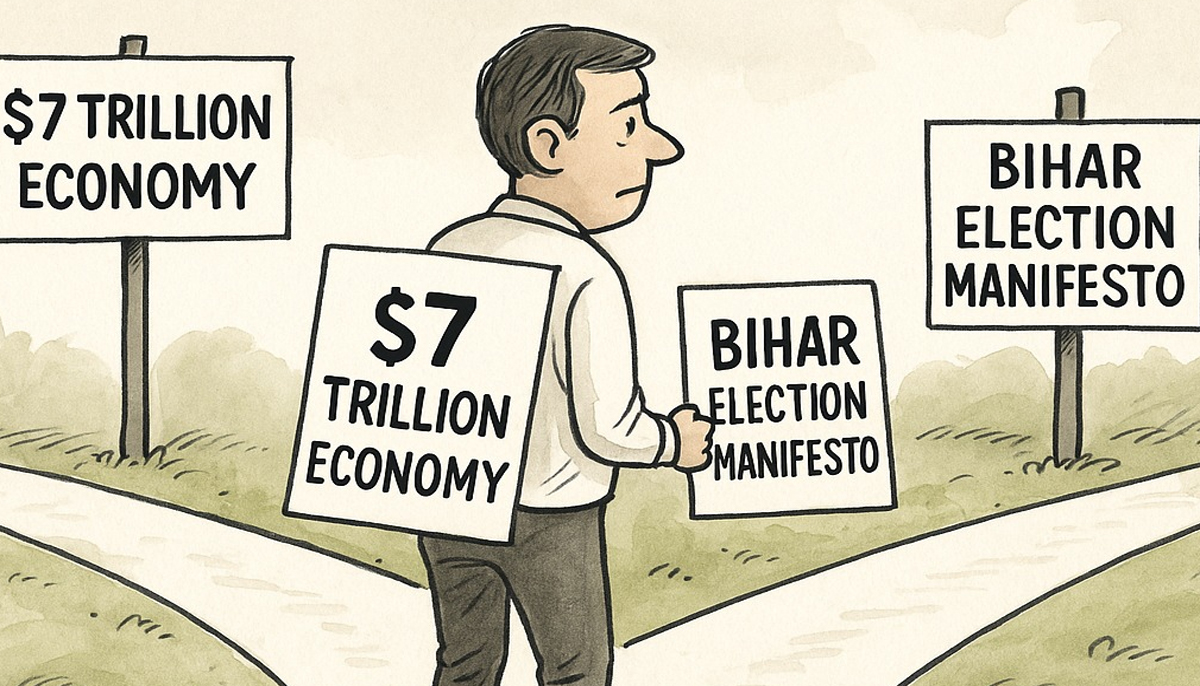

So here’s the final question: Will the Prime Minister steer India to a $7 trillion economy? Or will he, too, write another script for the next election? Will he nudge the 16th Finance Commission to quietly tilt the scales—just enough to fix the narrative before the Bihar elections?

This isn’t just about budgets—it’s about futures. Yours, mine, and our children’s. Politicians will survive a bad policy. But the rest of us have to live with its cost.

But maybe, just maybe, we still have time to stand tall.

The conversation must not end here. Let it begin.

Business and Economy

Business and Economy  Education

Education  Food

Food  Government

Government  Lifestyle

Lifestyle  Politics

Politics  Travel

Travel  World

World